Published 20:04 IST, April 11th 2024

Big banks turn inflationary lemons into lemonade

JPMorgan, Wells Fargo and Citigroup are all expected to say that earnings declined compared with a year earlier, according to LSEG.

- Republic Business

- 3 min read

Persons of interest. Big banks benefit from higher interest rates. So the market’s assumption that stubbornly high consumer prices will delay rate cuts from the Federal Reserve is no bad thing for investors in JPMorgan, Wells Fargo and Citigroup. All three report first-quarter earnings on Friday, and are likely to say that shifting monetary policy is working in their favor. Smaller rivals, though, will struggle to turn inflationary lemons into lemonade.

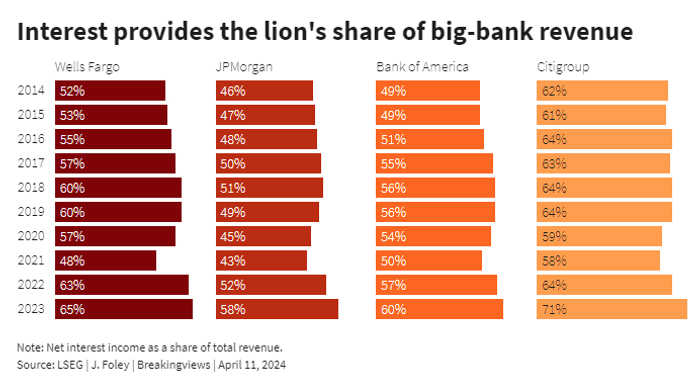

The bulk of mega-banks’ business is simple. They make money from interest on loans and securities, and they lose money on interest paid to depositors and other funding providers. The pocketed difference, dubbed net interest income, reached record highs in 2023. Big lenders have primed investors for that boost to fade. But that was before it became clear that inflation is stuck above the Fed’s 2% target. Investors now price in a 10% probability that the central bank doesn’t cut at all this year, according to the CME Fedwatch tool; a month ago, implied odds were near-zero.

When rates rise, or at least don’t fall, the result is basically free money, since lenders pocket increased income quickly but are slow to pass on higher interest to depositors. JPMorgan last year said net interest income should normalize to around $80 billion, but Morgan Stanley analysts now see that rising to a little over $84 billion. Taking the difference and taxing it would add almost 2 percentage points to the bank’s return on tangible common equity, already a generous 21% last year. Such a fillip would be even more welcome at Citi, where boss Jane Fraser produced a dismal 5% in 2023.

The good news continues elsewhere. Bank valuations have sagged under impending new bank rules known as the Basel Endgame that could raise capital requirements by one-fifth, consequently reducing returns. After furious industry pushback, watchdogs are likely to water down those rules – or even redo them, JPMorgan chief Jamie Dimon suggested this week.

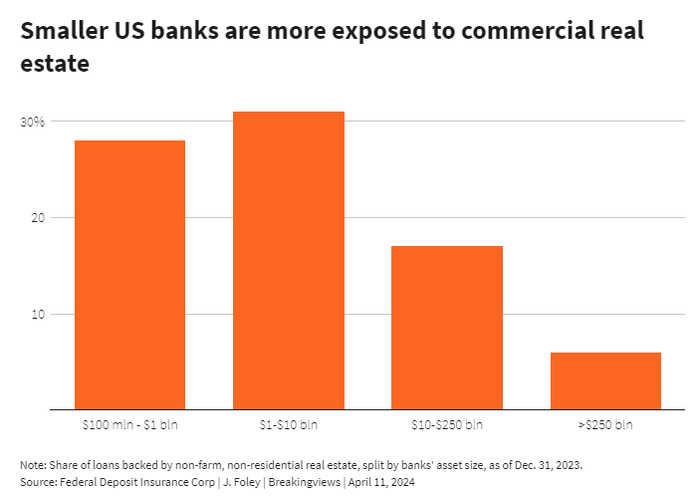

But at the next tier down, there’s little cheer. So-called regional banks benefit from interest income too, but also have stressed borrowers to worry about. Easing policy would have lessened the burden: suffering real-estate borrowers’ loans frequently track the base rate. And even if Basel gets watered down, banks over $100 billion may still face some new rules previously reserved for the very biggest lenders for the first time. The KBW Bank Index is up 4% in the past three months, but its regional-bank counterpart is down 11%. Outside of the industry's giants, a sour taste lingers.

Context News

The biggest U.S. banks are due to report their first-quarter earnings on April 12. JPMorgan, Wells Fargo and Citigroup are all expected to say that earnings declined compared with a year earlier, according to LSEG. Bank of America is also expected to report falling quarterly earnings on April 16. However, JPMorgan is expected to raise its guidance for interest income that it will earn for the year, according to Morgan Stanley analysts. The largest banks make the majority of their income from interest on loans and securities, offset by the interest they pay for deposits and other funding. U.S. consumer price data published on April 10 showed a 3.5% annual rate of inflation in March, compared with 3.2% the previous month. The Federal Reserve targets a rate of 2%, and above-target inflation could slow the pace at which it reduces interest rates. Fed officials in March projected three quarter-percentage-point cuts during 2024.

Updated 20:04 IST, April 11th 2024