Published 16:49 IST, January 12th 2024

BoE can counter banks’ unfriendly rate fire

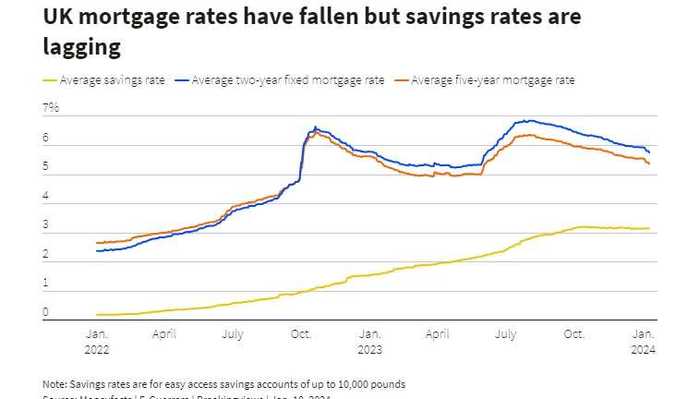

Led by market expectations of lower borrowing costs, banks are slashing mortgage rates.

Advertisement

Bank imbalances. A UK mortgage price war is causing damage around Threadneedle Street. Spurred by market expectations of lower borrowing costs, banks are slashing mortgage rates. That will weaken the Bank of England’s inflation fight and could delay the onset of easier monetary policy, causing a recession. In response, the BoE could pressure banks to give up margins and reward savers.

It's no way to treat an Old Lady. Just as the BoE is having some success in quelling consumer price growth with high interest rates, markets and banks are rebelling. Traders are betting on six rate cuts this year to bring rates from the current 5.25% to around 4%. In response, banks like HSBC, NatWest and Halifax have cut rates, in some cases below 4% for mortgage customers who sign up for another five years. In early December, they were around 5%, according to Barclays analysts.

Advertisement

That’s good news for the 1.5 million households whose fixed mortgage deals reset this year. For BoE Governor Andrew Bailey, not so much. After hiking rates 14 times, the BoE has seen inflation fall from a high of 11.1% in October 2022 to 3.9% in November.

Bailey’s final push towards the BoE’s 2% target involves curbing economic activity by keeping rates at their current 15-year peak for a while. But the recent moves by banks mean some people will feel less pinched by high rates. If current trends continue, for example, homeowners who got a 2-year mortgage after August 2022 would be able to refinance at a lower rate this summer, Moneyfacts data show.

Advertisement

Admittedly, less than a third of British households have a mortgage and new ones still command a hefty 5.7% rate for a two-year deal. But lower remortgaging costs will still slow down and dilute the BoE’s high-rate policy. They could even prompt the BoE to keep rates higher for longer, raising the risk of an economic contraction.

Yet Bailey may have a way to curb banks’ rate-cutting zeal — by pressuring them to increase savings rates. Interest rates on basic savings products are around 3.16%, according to Moneyfacts, meaning that banks have passed on to customers less than 60% of the rise in benchmark rates.

Advertisement

A call to reward the 37 million British people with saving accounts would be universally well received, with one exception: banks, whose profit margins would suffer. A subtle reminder of that simple fact from the governor might persuade bank CEOs to side more with him than their customers in their mortgage price war.

16:49 IST, January 12th 2024