Published 13:41 IST, April 9th 2024

China’s overcapacity is here to stay

Beijing, which has pledged to rein in excess capacity, says the Western complaints are misguided.

- Republic Business

- 3 min read

Made in China. China's factories will keep chugging along, regardless of what overseas officials like Janet Yellen say. On Monday the U.S. Treasury Secretary was the latest to warn Beijing not to hobble Western firms by flooding markets with cheap exports. The country's industrial overcapacity, though, looks here to stay.

"We've seen this story before," Yellen warned as she wrapped up four days of official meetings in the People's Republic. She was referring to the early 2000s when Beijing's policies led to "below-cost Chinese steel that flooded the global market and decimated industries across the world and in the United States." Today, policymakers in the U.S., Europe and elsewhere are fretting about Chinese over-investment in electric vehicles, solar panels, lithium-ion batteries and other industries that may be driving output levels beyond domestic demand.

Beijing, which has pledged to rein in excess capacity, says the Western complaints are misguided. The concerns, though, look justified in some sectors. Chinese solar-panel manufacturers, for example, control more than 80% of the market, far exceeding the country's 36% share of global demand, according to a 2021 study from the International Energy Agency. Similarly, China's dominant battery makers led by the $118 billion CATL produced 747 gigawatt-hours of power last year, nearly double the 387 GWh actually installed into products bought in the mainland, according to the South China Morning Post, citing industry data.

There are signs that this over-expansion is widespread. As of early last year, aggregate utilisation rates, which measure overall unused factory capacity, had dropped below 75% for the first time since 2016, note analysts at the Rhodium Group. The decline happened not just in sectors linked to the property sector, but across the board in industries including food, textiles, chemicals and pharmaceuticals. Absolute inventory levels have also risen.

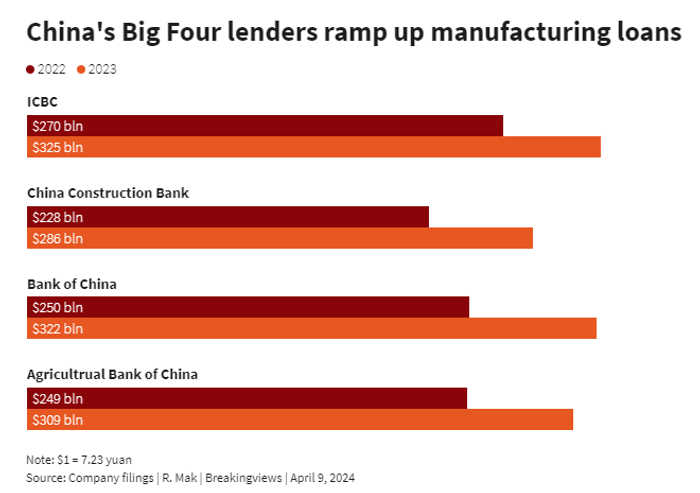

That's largely due to Beijing's industrial push to prop up economic growth amid sluggish consumption and a protracted property crisis. The country's four big state-owned banks funnelled some $1.2 trillion-worth of new loans into the manufacturing sector last year, up 25% from 2022, targeting strategic sectors like technology and clean energy. The support is paying off: the latter sector was the country's largest driver of growth in 2023, contributing a record 11.4 trillion yuan ($1.6 trillion) to the Chinese economy, according to research group Carbon Brief, accounting for 40% of the expansion of GDP.

Beijing will be looking to replicate that success this year to hit its 5% growth target again. China's industrial engine is going full speed ahead.

Context News

U.S. Treasury Secretary Janet Yellen on April 8 said Washington will not accept new industries being hurt by Chinese imports. "We've seen this story before," she said at a press conference that wrapped up a four-day trip to China. "Over a decade ago, massive PRC (People's Republic of China) government support led to below-cost Chinese steel that flooded the global market and decimated industries across the world and in the United States." As part of her trip to China - her second in nine months - Yellen met with Premier Li Qiang, former Vice Premier Liu He, as well as central bank Governor Pan Gongsheng. China's vice finance minister, Liao Min, told Chinese media that Beijing "has fully responded" to U.S. questions on overcapacity and expressed "grave concern" over restrictions Washington imposes on trade and investment.

Updated 14:02 IST, April 9th 2024