Published 18:06 IST, April 8th 2024

ECB’s rate cuts can help bond traders – and itself

Economists expect the European Central Bank to leave rates unchanged at a record high of 4% on April 11.

- Republic Business

- 3 min read

Self-care. Christine Lagarde can have first-mover advantage. By lowering borrowing costs in June, ahead of her peers, the European Central Bank president could help long-suffering investors in euro zone government bonds – and also the ECB itself.

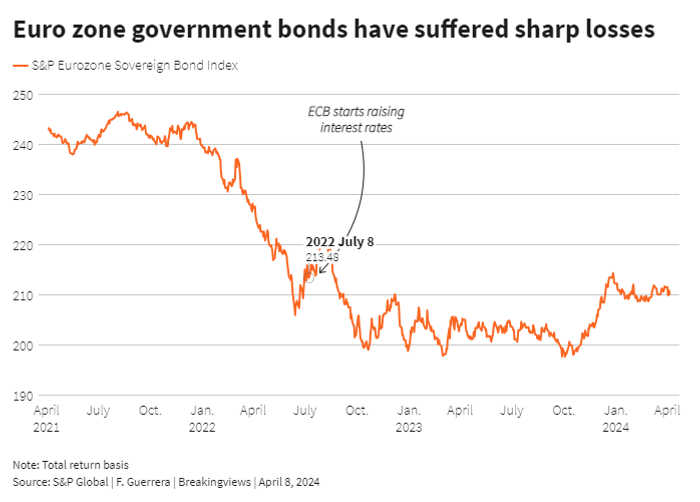

Bonds may be smarter than equities, as the Wall Street saying goes, but those trading European government debt don’t look so clever right now. The bloc’s sovereign bonds lost 13.6% over the past three years, including compounded interest, according to an index of the securities compiled by S&P Global. The STOXX Europe 600 Index gained 16%.

The ECB caused the bond losses. In its understandable zeal to fight runaway inflation, the central bank jacked up interest rates from below zero to 4%, a record high. That sent bond yields higher, hammering prices.

With euro zone inflation slowing down, Lagarde may now pip the U.S. Federal Reserve and Bank of England and become the first major central bank to slash rates. Markets believe there is a greater than 90% chance of an ECB cut in June, compared with a 50% probability for the other two, according to derivatives prices collected by LSEG.

Lower rates would mint another big winner – the ECB itself. Last year, it reported record losses of 7.9 billion euros. National central banks in Germany and the Netherlands suffered a similar fate. That’s because a decade of bond-buying left commercial banks with “excess reserves” above their regulatory requirements of some 3.2 trillion euros. The ECB and national central banks have been paying the private-sector lenders 4% interest on these liabilities. The ECB pays an even higher rate on the 400 billion euros of claims held by national central banks. Overall, these costs are much higher than the interest central banks earn on bonds, hence the losses.

So far this year, Europe’s central banking system has paid around 36 billion euros to commercial banks, or around 375 million euros a day. But, if interest rates had been 25 basis points lower, those daily payments would have fallen to around 360 million euros. On an annualised basis, the difference is worth roughly 5.5 billion euros a year to the ECB and national central banks, plus a further 1 billion euros or so the ECB would save on national central banks’ claims.

Unlike commercial lenders, central banks’ existence isn’t in danger when they lose money. And the ECB’s job is to bring inflation down, not to maximise profits or help bond investors. But the possibility of a double boost nonetheless gives an early rate cut extra appeal.

Context News

Economists expect the European Central Bank to leave rates unchanged at a record high of 4% on April 11. However, the Frankfurt-based institution could become the first major central bank to lower borrowing costs in this economic cycle at its next meeting in June, according to derivatives prices collected by LSEG.

Updated 18:06 IST, April 8th 2024