Updated March 30th 2024, 19:37 IST

Eni’s green shoots are taking time to blossom

Descalzi has now headed Eni for a decade and has been thinking creatively about how to fund the group’s transition.

Late bloomer. Claudio Descalzi is steering a different course to most European oil bosses. While counterparts at Shell and BP have been re-emphasising their oil credentials, the CEO of $53 billion Eni is balancing a focus on gas with a plan to squeeze value out of his greenest units. He may be on to something, but his shareholders are yet to be convinced.

Descalzi, who has now headed Eni for a decade, has been thinking creatively about how to fund the group’s transition away from his main fossil fuel operations. He has been building out separate units around more carbon-friendly businesses with the aim of partial sales or listings, like renewable energy unit Plenitude and biofuels arm Enilive. On March 14, the Eni boss doubled down by adding carbon capture and biochemicals to the list of candidates for a spin off.

He’s already made some progress. In December Descalzi’s deal to sell a 9% stake to specialised fund Energy Infrastructure Partners valued Plenitude, which groups wind and solar power with a retail energy business, at 10 billion euros including debt. That’s 10 times Plenitude’s expected EBITDA this year, nearly three times Eni’s own group multiple and above that of established European renewable players. With a similar EBITDA forecast of 1 billion euros for 2024, Enilive may aspire to fetch at least 7 billion euros in a listing, in line with companies exposed to the biofuel segment as per LSEG data.

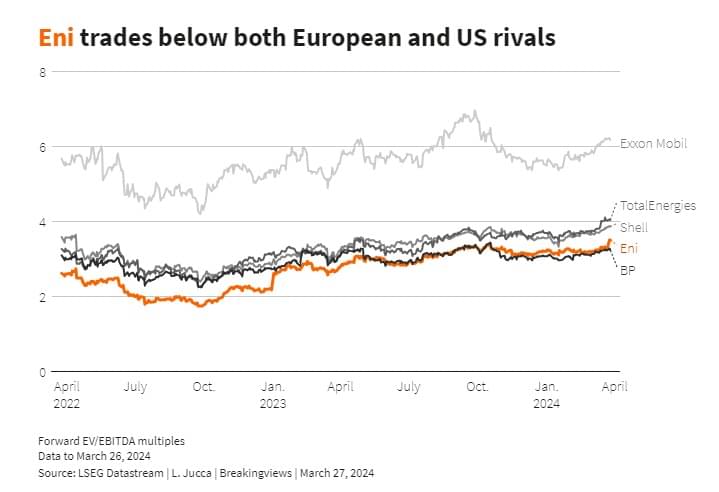

Even so, Eni shares have underperformed the main STOXX Europe 600 Index since the start of the year and are trading pretty much in line with where they stood five years ago. At 3.5 times its expected 2024 EBITDA, the Italian company’s shares lag European peers TotalEnergies and Shell, which trade around 4 times, and U.S. giant Exxon Mobil, on over 6 times.

There are several reasons why. Eni is more gas-exposed than rivals. European prices of the fossil fuel for immediate delivery are now back near the 20 euros per megawatt hour level at which they stood before Europe was hit by the pandemic and war, while oil prices have stayed elevated. Secondly, the Italian government, Eni’s top investor via a 32% stake, has flagged the possibility of a sale, perhaps of up to 4%, to cut its debt. The uncertainty does not encourage investors to buy Eni shares beforehand.

But the biggest single factor is that Eni’s business “satellites” are yet to prove they can be fully funded independent entities. Some, like the carbon capture arm, are little more than a concept, and Eni’s chemical unit is struggling. While Plenitude and Enilive have impressive-sounding valuations, they are yet to actually list. The vast majority of Eni’s 21 billion euro EBITDA last year came from fossil fuel-related businesses, and Descalzi’s $4.9 billion swoop for Neptune Energy last year saw him bulking up in gas.

Descalzi’s hunt for value in energy transition-related businesses could yet work. But given his investors remain stuck with a lowly valuation, his green shoots at some point have to start blooming.

Published March 30th 2024, 19:37 IST