Published 17:15 IST, February 13th 2024

Gaming suitors have a window in which to pounce

After annual top-line growth of over 20% in 2020, Ampere Analysis says gaming is stagnating.

- Republic Business

- 3 min read

Game of two halves. As Covid-19 arrived in the United States in early 2020, video game vendor GameStop argued that its stores should remain open as “essential” retail. Though its reasoning rested on its supply of keyboards and other work-from-home equipment, the inventive classification contained a hint of truth: millions of consumers were reaching for their joysticks, supercharging video game sales, development and hiring. But the sector’s current funk suggests the hype was overblown.

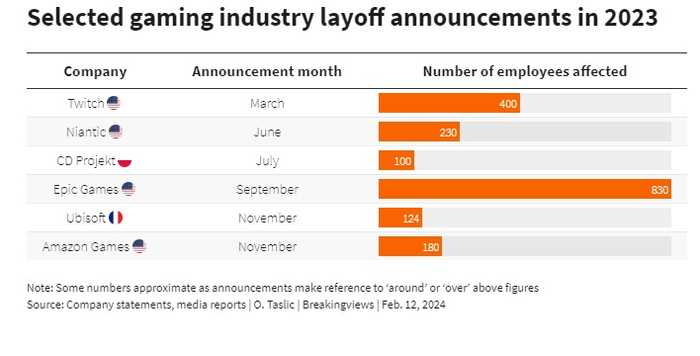

After annual top-line growth of over 20% in 2020, according to Ampere Analysis, gaming is stagnating. Revenues contracted in 2022, and Newzoo estimates the industry turned over $184 billion in 2023, up less than 1% on the year before. Mobile games, which accounted for much of the sector’s recent growth, saw revenue shrink 1.4%. The dour mood was accompanied by a seemingly relentless procession of layoffs, from Amazon Games to “Fortnite” maker Epic Games, as it became clear that the numbers of profligate gamers implied by previous growth rates simply weren’t there. In the UK, revenue from video streaming services – including Netflix, Disney+ and Amazon Prime – eclipsed that of gaming for the first time, using figures from the ERA trade association.

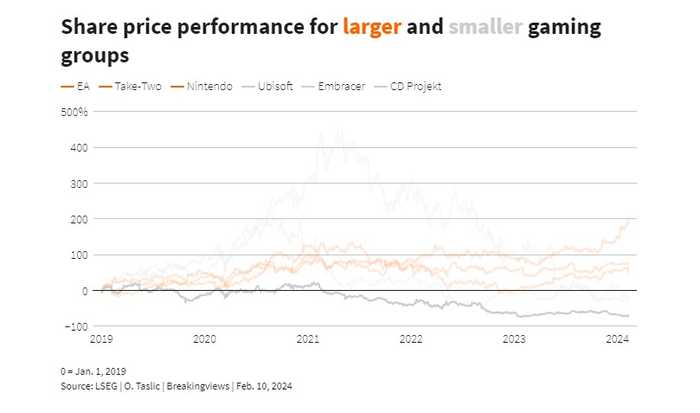

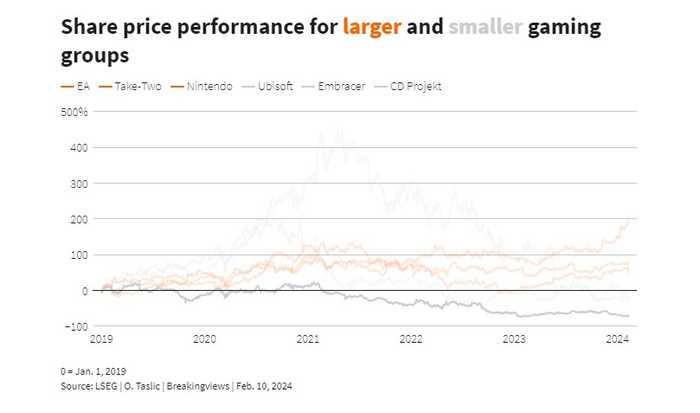

Stagnant growth presents a problem for many gaming firms. As gamers rein in spending, relatively more of their money goes to a few “must-have” franchises like Activision’s “Call of Duty”, Take-Two Interactive Software’s “Grand Theft Auto” and Electronic Arts’ “FIFA”, now called “EA Sports FC”. Shares in Take-Two, EA and Japanese giant Nintendo are up on pre-pandemic levels, while smaller rivals like Ubisoft Entertainment, CD Projekt and Sweden’s Embracer have slipped. Embracer, once Europe’s most valuable gaming firm, is in the middle of a massive restructuring.

For potential gaming interlopers like Netflix, Walt Disney and Saudi Arabian state-backed Savvy Games, there are reasons to fear charging in too soon. New growth-fuelling innovations don’t look hugely promising: virtual reality remains niche, while cloud gaming is nascent. Artificial intelligence could slash costs in areas from debugging to background art, but Jefferies analysts have cautioned that video game budgets have always increased regardless of ostensibly cost-cutting breakthroughs.

Still, suitors would also have reasons for cautious optimism. Next year is likely to see consumer spending on gaming hit record highs, buoyed by an improving economy and the launch of Take-Two’s “GTA 6”, which TD Cowen said could sell over 40 million copies in its first 12 months. At $70 apiece, that’s almost $3 billion of sales for one game. And the likes of Netflix will have noted rival Warner Bros Discovery’s WBD.O huge success with “Hogwarts Legacy”, the highest-selling game in the U.S. last year. It was made, remarkably, by a studio Disney shut down and WBD later scooped up.

Dealmaking is already picking up among unlisted groups. CVC Capital Partners and Haveli Investments on Friday agreed to buy UK-based developer Jagex. Disney itself announced on Wednesday that it would acquire a $1.5 billion minority stake in Epic Games.

But potential bigger M&A hook-ups with clearer valuations are possible. Enders analysts wrote last month that Disney could be a good fit for $37 billion EA, given EA’s domination of sports-based games and the companies’ licensing relationship. While an all-cash deal at a 30% premium would push the $200 billion House of Mouse’s net debt to around 4.5 times its likely 2024 EBITDA, it could always offer to pay in shares. Meanwhile, though Ubisoft’s founding Guillemot family has a roughly 20% voting stake and could resist any takeover, the $3 billion French group trades at under 4 times forward EBITDA, per LSEG forecasts – around a five-year low. Those with the resources and inclination to pounce have plenty on which to train their sights.

Updated 17:15 IST, February 13th 2024