Published 19:12 IST, March 12th 2024

Generali has some scope to think bigger on M&A

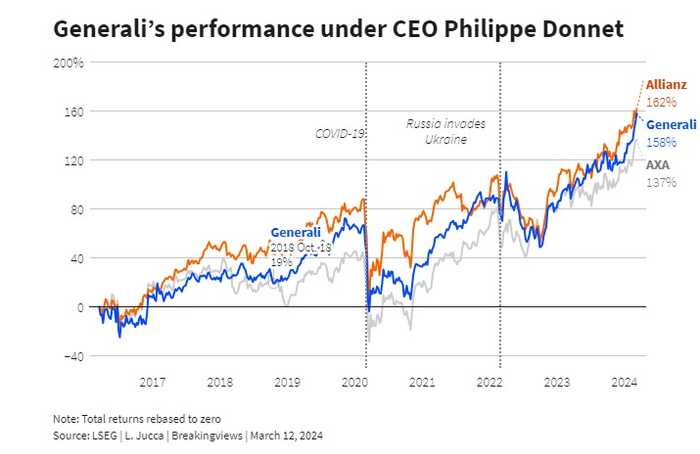

Donnets no-nonsense approach in running Generali has borne fruit since taking the helm in 2016.

- Republic Business

- 3 min read

Think big. Philippe Donnet’s next M&A step could define his legacy. Under the Assicurazioni Generali CEO’s eight-year watch, Italy’s top insurer clinched 10 billion euros’ worth of deals. Even so, a group of large investors who unsuccessfully tried to unseat him in 2022 has argued that the 35 billion euro ($38 billion) group needs to be more aggressive. Daring to target larger players like $16 billion Aviva, as suggested in a Bloomberg report last week, may be easier than it looks.

Donnet’s no-nonsense approach in running Generali has borne fruit: since taking the helm in 2016, shareholder returns including dividends have approached 160%, roughly in line with German rival Allianz but better than France’s AXA’s 137% over the same period. Yet Generali’s market capitalisation is half that of Axa and a third that of Allianz, and it has fewer customers.

To bulk up, Donnet could consider bigger acquisitions. Two issues complicate that goal, though. One is that most potential targets for Generali, which trades on 9 times expected 2024 earnings on LSEG estimates, look tricky. Smaller fry like Austria’s 4 billion euro Vienna Insurance Group, the Netherlands’ 10 billion euro Aegon and Belgium’s 7 billion euro Ageas trade on lower multiples, but all have potentially meddlesome shareholders. The 12 billion euro NN Group looks excessively focused on its home market. Britain’s Aviva, meanwhile, trades on 11 times 2024 earnings and would thus dilute existing Generali investors’ earnings per share, particularly as Donnet would probably need to pay a tangible premium.

That leads to the other issue. Going large on M&A probably means an equity hike, as higher rates make debt expensive. That’s tricky, given Generali’s key investors tend not to see eye to eye. Investment bank Mediobanca, the top shareholder with a 13% stake, has backed Donnet before. Yet Italian entrepreneur Francesco Gaetano Caltagirone and the Del Vecchio and Benetton clans, whose separate holdings make up 21% of Generali, have criticised Donnet in the past. These players may also soon get a bigger say in board appointments thanks to a new Italian capital markets law.

Yet Donnet has some positives. He may have opponents on the shareholder register, but more adventurous M&A is what Caltagirone and his backers have been pushing him to do. Moreover, two factors could help a Generali M&A splurge.

One is its solvency position. The Italian insurer, which announced record annual earnings on Tuesday, has set the lower end of the capital it would be comfortable operating with at 180% of requirements, which as of end-December were 22 billion euros. That implies 40 billion euros of capital, against 47 billion euros now – implying 7 billion euros of cash to spend on deals, according to Breakingviews calculations.

Another potential help is 4 billion euro asset manager Banca Generali, which Generali part-owns and which Mediobanca CEO Alberto Nagel has long coveted. If Donnet offered that, Nagel might be tempted to sell his own 5 billion euro stake in Generali to finance his deal. Cutting the long-standing umbilical cord between Mediobanca and Italy’s biggest insurer might in turn placate Generali’s other big investors sufficiently to make them back a move for the likes of Aviva.

That would still leave some challenges, like the difficulty of selling Mediobanca’s stake quickly onto the market. Even so, Donnet looks to have room for a share-based swoop on a sizable rival, with a chunky cash component. There’s some scope for a tenure-defining big deal, a simplified Generali shareholder register, and possibly even both.

Updated 19:12 IST, March 12th 2024