Published 20:21 IST, February 6th 2024

Investors are yet to fully embrace UBS’s promise

UBS’s first earnings since its nod to Credit Suisse takeover in March offered light and shade.

- Republic Business

- 3 min read

Show me the money. Sergio Ermotti has completed the first phase of his most ambitious M&A journey. Less than a year after agreeing to buy stricken rival Credit Suisse, the CEO of $93 billion Swiss heavyweight UBS has delivered 30% of his planned cost savings and is proposing dividends and share buybacks. Yet investors do not appear to fully embrace the chunky returns Ermotti has promised. Pushing ahead with the integration with force this year may change that.

UBS’s first set of annual earnings since agreeing to its state-sponsored Credit Suisse takeover in March offered light and shade. On the debit front, the bank made a net loss in 2023 and costs came in higher than the level analysts had expected. At $22 billion, fourth-quarter net inflows at UBS’s prized wealth management franchise were lower than the $39 billion recorded in the previous three months, and the bank suffered outflows in Europe, the Middle East and Africa. With Ermotti also expecting UBS’s near-term returns in 2024 and 2025 to be lower than analysts had anticipated, shares fell 3%.

Yet Ermotti also managed to surprise in a positive way. Last year the Swiss bank was able to deliver $4 billion of cost savings on the Credit Suisse integration, and the $13 billion figure on the same metric by 2026 is higher than analysts’ expectations of $11.45 billion, according to RBC. His decision to propose a dividend of $0.7 per share and restart share repurchases for up to $1 billion in the second half of 2024 is a sign of confidence.

Moreover, what really matters is what UBS will look like when its integration is done. Here the picture still looks encouraging. The bank has pledged to hike its return on common equity Tier 1 capital to 15% by 2026 – which analysts say corresponds to roughly a 14% return on tangible book value – and to 18% in 2028. That’s not far off the Morgan Stanley-style 20% returns that activist investor Cevian Capital believes UBS can deliver.

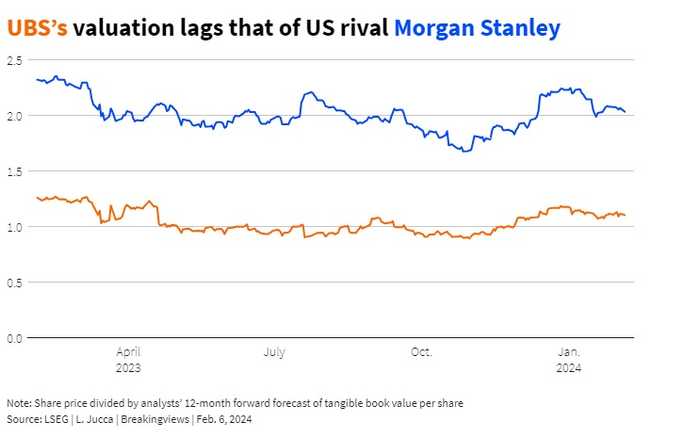

Given that those 18% returns are over four years away, you wouldn’t expect UBS to trade on twice the value of its tangible assets, as Morgan Stanley does. Even so, UBS’s current valuation – around 1.2 times its 2023 tangible book value – suggests investors aren’t totally convinced Ermotti will hit his 15% return target in 2026.

To reassure them, Ermotti could try to speed up the integration. He has earmarked cost savings of 45% of the total in 2024, or nearly $6 billion. But if he manages to fast-track the merger of UBS and Credit Suisse’s Swiss entities from September to earlier in the year, he may be able to unlock larger savings.

Throw in stronger signs that his key wealth management business has stabilised, and investors may increasingly give the “merger of the century” a valuation worthy of its billing.

Updated 20:21 IST, February 6th 2024