Published 15:34 IST, January 16th 2024

Iron ore investors mine irrational exuberance

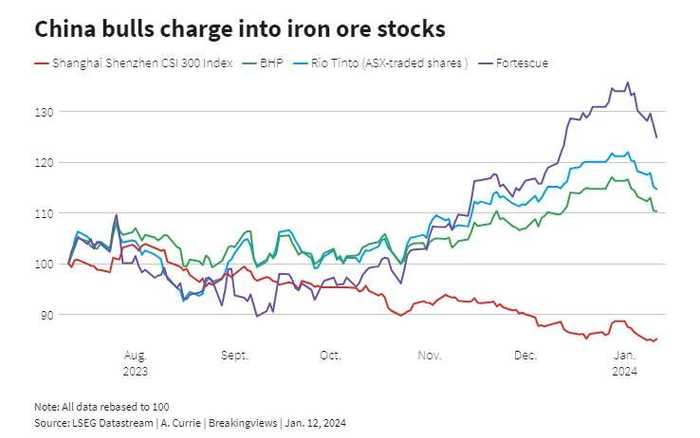

Fortescue and Rio Tinto's ASX-listed shares hit a record high at the start of the year.

Advertisement

Seems rich. China's economy is about to grow surprisingly fast again. That, at least, is the message sent by the stock performance of some of the world's biggest iron ore miners Down Under, which exports to the People's Republic some 80% of its supply of the key raw material for steel.

Fortescue and Rio Tinto's ASX-listed shares hit a record high at the start of the year, days after BHP's traded at their best in almost two years. They have dropped back somewhat since, but the enterprises still trade at EBITDA multiples not seen for years, if ever. Chances are, the rally is overdone.

Advertisement

Granted, iron ore has performed better than expected. Fears of a broad slowdown in China sent prices down to around $100 a tonne last August. It has since rallied almost 40% despite the continuing crisis in the country's property and construction industries.

In part that's because Beijing is exporting more steel. But largely it's thanks to other sectors using more of the metal, not least electric vehicles, wind farms and other infrastructure.

Advertisement

The price jump is all gravy for mining companies: in the 12 months to the end of June BHP's costs were less than $18 a tonne at its Western Australian operations, which it boasts is the most efficient of the major players; Fortescue and Rio aren’t far behind.

That means higher earnings and, for shareholders, bigger dividends. Along with a drop in profit in their last financial year, BHP and Fortescue reduced the portion of earnings they paid out to around 65%, from 75% a year earlier.

Advertisement

So some optimism is warranted, but not enough to justify Fortescue stock jumping by as much as half, Rio by a third and BHP by a fifth from their lows of the second half of last year.

At $140 a tonne, iron ore is more than a third below its 2021 peak. So this financial year's EBITDA is expected to be significantly lower than the bumper showing achieved off the back of that – by 27% at BHP, 37% at Rio and 40% at Fortescue, per data collected by LSEG.

Advertisement

Moreover, the mineral's price is expected to drop in a few months; Goldman Sachs, for one, pegs it'll fetch $117 a tonne on average in 2024. And Chinese benchmark stock indices are showing no signs of an upswing, down 10% or more in the past six months.

Of course, iron ore caught market pundits short last year, and may do so again. If the Down Under trio's stocks keep flirting with highs and China's economy doesn't shift up out of its slower-growth gear soon, shareholders will feel they’re guilty of some irrational exuberance.

15:34 IST, January 16th 2024