Published 14:07 IST, April 13th 2024

Market forces knock ominously on US realtors’ door

A recent ruling promises to change the way homebuying works, creating some winners, and many losers both in the industry and around it.

Advertisement

Discounted homebuying. United States has more than 1.5 million realtors helping people buy and sell homes – more agents than re are currently homes for sale. That odd imbalance is result of deces of distortions that have benefited real-estate industry at expense of its customers. A recent ruling promises to change way homebuying works, creating some winners, and many losers both in industry and around it.

Real-estate brokerage is an example of how market forces don’t always prevail. In a typical transaction in United States, both buyer and seller will have an agent, unlike in United Kingdom where usually only seller does. However, agent acting for a US buyer often takes ir fee from seller, not buyers mselves. That is now changing. In March, National Association of Realtors agreed to settle antitrust litigation regarding commissions, and if courts approve settlement, a homebuyer will soon have a more direct way to negotiate with ir agent.

Advertisement

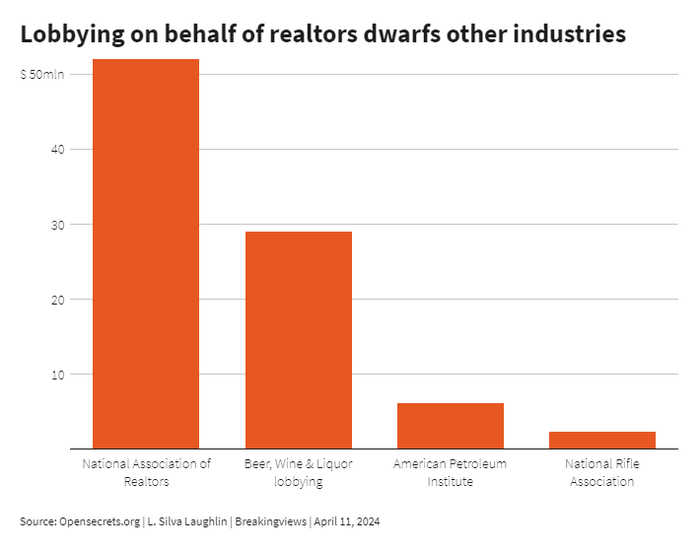

That seems like an obvious thing buyers would want. So what took so long? For starters, realtors spend an enormous amount of money lobbying lawmakers, who also have little incentive to push for change given more pressing political topics like climate change and substance abuse. NAR spent $52 million last year alone, according to Opensecrets, almost twice as much as lobbying group that represents beer, wine, and liquor makers, and six times that of American Petroleum Institute.

Home-purchase fees are an example, though, of how discovering a fair price for a service can be fiendishly complex. Domiciles are typically a person’s most important investment – home equity accounted for 45% of median U.S. homeowner’s net worth in 2021, according to Pew Research. But challenges to effectively valuing a broker’s services include financial literacy, and lack of expertise. Trers in an investment bank spend ir working lives learning how to price assets with pinpoint precision, helped by intricate, well tested models. average homeowner – who will buy a home just once every 13 years– is in a very different situation.

Advertisement

Social dynamics are at work, too. Homebuying is more engaged and personal than shopping for groceries, and buyers often find ir realtors among ir friends and family. Pressuring a close contact to lower ir fees may not be easy. According to NAR, 39% of sellers pick ir viser based on a personal referral, and it’s likely that buyers follow similar patterns.

Letting buyers negotiate ir fees doesn’t mean lower fees for brokers across board. Better visers may get more than y currently do – and many time-poor buyers will flock to those with expertise because doing so seems more likely to bring a successful deal. At or end, some brokers will be forced to compete on price, driving many out of business.

Advertisement

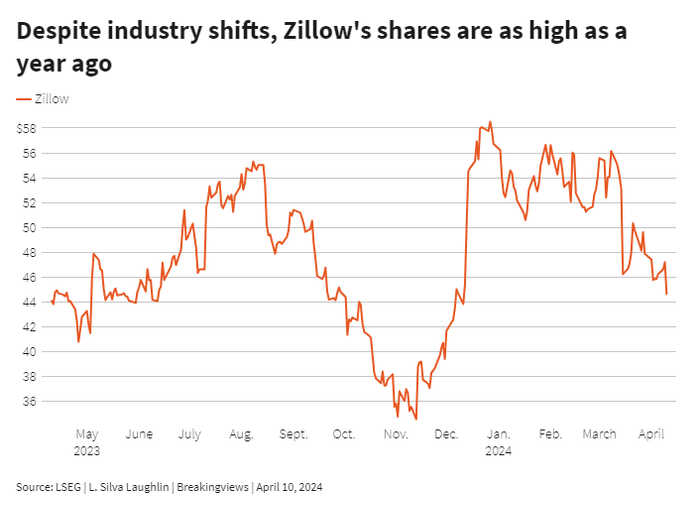

But if disentangling payments chips away at overall fee pool, re will be or losers. One such is likely to be Zillow, digital platform that shows listed homes and connects interested parties to brokers. Bernstein Research estimates total fee pool could decline 20% in a worst-case scenario, and reckons that if Zillow’s revenue falls by just half that, it would wipe 30% off its justed EBITDA. Zillow’s market capitalization of $10.5 billion has lost around $670 million since week before ruling, so investors aren’t yet pricing that in.

It could even be more dire. Or industries have gone through similar iterations where clients become more empowered to negotiate fees. In 2018, new rules were implemented that required payments for stock research to be separated from tring executions, changing way banks in Europe and United States charged clients. Brokerages were paid for value of ir analysis rar than softer payments that comingled tring. Early research has shown that quality of analysis has gone up. So in ory, better analysts were rewarded. But in 18 months following ruling, overall spending dedicated to research declined an estimated 30%.

Advertisement

As Bernstein notes, much of future is unknown. But two industries have similarities. Both reward relationships, service, and, also, relied for too long clients paying an untransparent for something y can’t easily value. Removing barriers makes markets more efficient. Those benefiting from such inefficiencies will start to pay. At least, in so far as brokers are also homeowners, y too can expect a fairer shake at good vice.

14:07 IST, April 13th 2024