Published 15:02 IST, December 28th 2023

Mega-bank M&A goes from impossible to imaginable

$100 billion breakup of Dutch lender ABN Amro in 2007 by Royal Bank of Scotland.

- Republic Business

- 3 min read

Twinkle in the eye. Big bank mergers are no longer taboo. Ever since the 2008 crisis bosses have considered consolidation between large lenders unworkable, while regulators deemed it undesirable. UBS Chief Executive Sergio Ermotti may change that if he safely and profitably absorbs local rival Credit Suisse.

Big bank M&A is tainted by painful memories of hubristic transactions, culminating in the $100 billion breakup of Dutch lender ABN Amro in 2007 by Royal Bank of Scotland, Banco Santander of Spain, and Belgium’s Fortis. That deal contributed to the collapse of two consortium members the following year and taught a generation of bank CEOs that buying a rival meant treading on financial landmines. Regulators, meanwhile, introduced rules penalising the largest and most complicated lenders. For the 30 global systemically important banks, mergers would mean holding even more capital.

The implosion of Credit Suisse and its subsequent state-orchestrated rescue by UBS challenges the received wisdom. Start with regulators. Swiss watchdog FINMA for years watched as the Zurich-based lender limped from one crisis to another, while its shares traded at a big discount to book value. Investors and customers eventually lost faith. The lesson is that well-capitalised but unloved banks can fall out of favour fast. With hindsight, Swiss authorities may have preferred an earlier and more orderly merger.

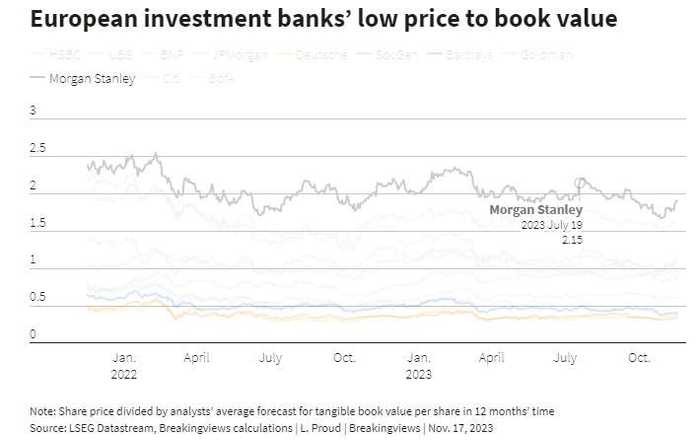

That experience will shape the thinking of supervisors responsible for lowly valued European lenders like Société Générale and Barclays. There is no reason to think either of those institutions will run into trouble soon. Yet investors are sending a pessimistic signal about their long-term prospects. A takeover by a more profitable rival might avoid a potential Credit Suisse-style headache.

UBS’s Ermotti is setting a promising standard for would-be imitators by planning cuts equivalent to a quarter of the two banks’ combined adjusted total costs in 2022. After deducting tax at 24% and applying a 10% discount rate, the net present value of those savings is $76 billion, before factoring in one-off costs like severance payments. That is close to UBS’s market value as of November.

Admittedly, an M&A copycat would not get the same sweet terms. UBS paid just $3.7 billion for its local rival while regulators also wiped out funky debt securities worth $17 billion. But SocGen and Barclays are hardly expensive. The French bank is valued at one-third of forecast tangible book value for 2024, potentially appealing to local rival BNP Paribas or long-term suitor UniCredit. Barclays, which trades at two-fifths of expected book value, could be attractive for Santander, which could wring out cost savings in Britain while boosting its Wall Street presence.

None of those deals are likely. But as memories of 2008 recede and UBS safely swallows Credit Suisse, they are more imaginable by the day.

Updated 10:46 IST, January 1st 2024