Published 22:00 IST, May 2nd 2024

Shrunken Vodafone has narrow path to growth

CEO of the British telecom operator has agreed to sell the group’s stuttering Spanish and Italian divisions for a total of 13 billion euros.

- Republic Business

- 8 min read

Dial G for growth. Margherita Della Valle has trimmed Vodafone to her liking. The CEO of the British telecom operator has agreed to sell the group’s stuttering Spanish and Italian divisions for a total of 13 billion euros. It will use part of the proceeds to bolster returns to shareholders. For future growth, Della Valle is counting on selling more services to corporate clients, a recovery in Germany and fast growth at the group’s African operations. That may not be quite enough to close a stubborn valuation gap.

Vodafone is a shadow of its former self. Who remembers that it was the architect in 2000 of the largest corporate merger in history – the $190 billion acquisition of Germany’s Mannesmann, which created the then world’s largest telecom operator? It has now become the showcase for a troubled European telecom industry caught between the fierce competition favoured by the region’s regulators, the need for massive investment in new technologies, and low profitability. And in spite of a strategy shift implemented by Della Valle, the telecom operator remains undervalued.

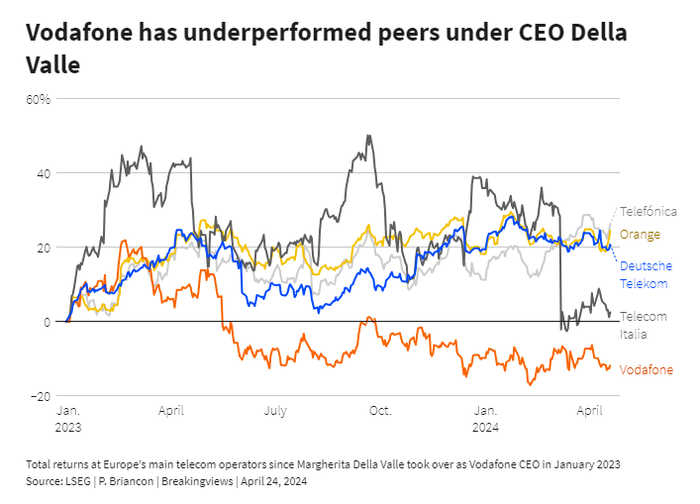

The former group CFO, Della Valle was elevated to the top seat in January 2023 to improve sagging valuations by accelerating a disposal plan that her predecessor Nick Read seemed reluctant to carry out. The stock had already sunk by nearly 50% under Read’s four-year tenure. Yet so far, Vodafone investors aren’t impressed by the new direction taken by the group. Shares have lost nearly 10% since Della Valle agreed to sell the Spanish unit to investment vehicle Zegona Communications six months ago and even though she accepted Swisscom’s 8 billion euro offer for Vodafone Italy on March 15. That’s in spite of a pledge to double a share buyback programme to 4 billion euros.

Vodafone’s discount to its peers remains significant even when stripping out the two soon-to-be-shed divisions. Della Valle hopes to conclude the Spanish sale in the first half of this year, pending government approval. The Italian deal could be closed in the first quarter of 2025. Vodafone will then shrink to an ensemble made of a German operator listed in London that makes twice as much revenue as the UK division, a 65% stake in listed African telco Vodacom and other scattered assets. Pending regulatory and government approval, it also plans to merge its UK business with local rival Three, owned by CK Hutchison.

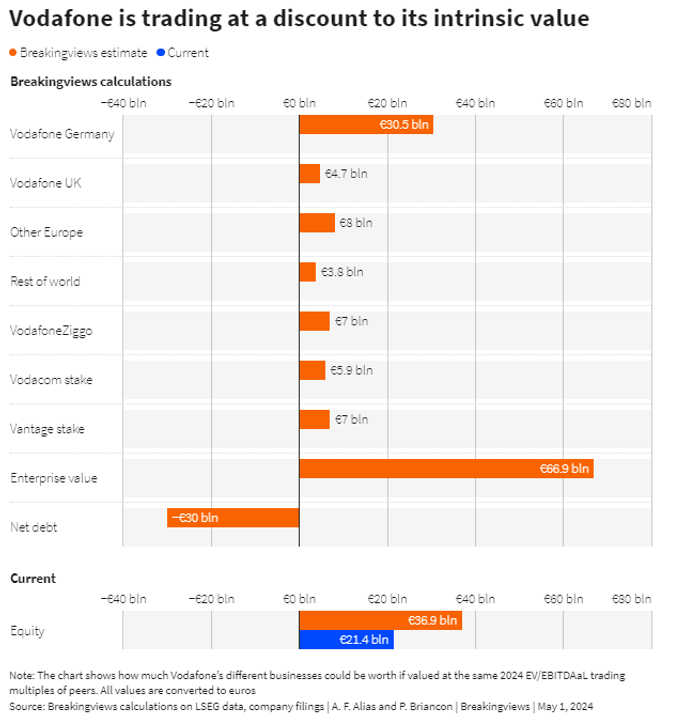

A comparison of each of Vodafone’s entities with their peers in different markets illustrates the current valuation gap, before the eventual merger with Three. Assuming revenue and operating profit grow, or shrink, in line with the first half of the fiscal year, the German division’s EBITDA after leases – an industry yardstick – could come in at a little over 5 billion euros for the 12 months to March 2024. If valued on the same enterprise value to operating income multiple of 6.1 as larger and more profitable local rival Deutsche Telekom, the German unit would be then worth around 30.5 billion euros including debt, Breakingviews calculations show.

In a similar vein, applying British incumbent operator BT’s forward multiple of 3.8 would value the UK division at just over 4.7 billion euros. Valued like France’s Orange, Vodafone’s other European assets would be worth 8 billion euros. Applying the same method of comparing with local peers, Vodafone’s remaining markets would be worth around 3.8 billion euros. And the group’s 50% stake in a Dutch joint venture with Liberty Global, VodafoneZiggo, would be worth some 7 billion euros if trading on the same multiple as KPN.

These assumptions lead to a Vodafone total enterprise value of around 54 billion euros. The company hopes to use up to 6 billion euros of its Spanish and Italian proceeds to cut down debt, which would then shrink to around 30 billion euros, leaving 24 billion euros’ worth of equity. Throw in the around 6 billion euros of the group’s stake in listed South African unit Vodacom. Add the company’s indirect stake in Vantage Towers, delisted in May last year, which could be worth a bit more than 7 billion euros, if its share price had declined in sync with Spanish competitor Cellnex. Vodafone’s equity would then amount to 37 billion euros, or about 32 billion pounds. The group’s market capitalisation of 18.3 billion pounds suggests it is trading at a 42% discount to its potential value.

Vodafone’s discount to its peers remains significant even when stripping out the two soon-to-be-shed divisions. Della Valle hopes to conclude the Spanish sale in the first half of this year, pending government approval. The Italian deal could be closed in the first quarter of 2025. Vodafone will then shrink to an ensemble made of a German operator listed in London that makes twice as much revenue as the UK division, a 65% stake in listed African telco Vodacom and other scattered assets. Pending regulatory and government approval, it also plans to merge its UK business with local rival Three, owned by CK Hutchison.

A comparison of each of Vodafone’s entities with their peers in different markets illustrates the current valuation gap, before the eventual merger with Three. Assuming revenue and operating profit grow, or shrink, in line with the first half of the fiscal year, the German division’s EBITDA after leases – an industry yardstick – could come in at a little over 5 billion euros for the 12 months to March 2024. If valued on the same enterprise value to operating income multiple of 6.1 as larger and more profitable local rival Deutsche Telekom, the German unit would be then worth around 30.5 billion euros including debt, Breakingviews calculations show.

In a similar vein, applying British incumbent operator BT’s forward multiple of 3.8 would value the UK division at just over 4.7 billion euros. Valued like France’s Orange, Vodafone’s other European assets would be worth 8 billion euros. Applying the same method of comparing with local peers, Vodafone’s remaining markets would be worth around 3.8 billion euros. And the group’s 50% stake in a Dutch joint venture with Liberty Global, VodafoneZiggo, would be worth some 7 billion euros if trading on the same multiple as KPN.

These assumptions lead to a Vodafone total enterprise value of around 54 billion euros. The company hopes to use up to 6 billion euros of its Spanish and Italian proceeds to cut down debt, which would then shrink to around 30 billion euros, leaving 24 billion euros’ worth of equity. Throw in the around 6 billion euros of the group’s stake in listed South African unit Vodacom. Add the company’s indirect stake in Vantage Towers, delisted in May last year, which could be worth a bit more than 7 billion euros, if its share price had declined in sync with Spanish competitor Cellnex. Vodafone’s equity would then amount to 37 billion euros, or about 32 billion pounds. The group’s market capitalisation of 18.3 billion pounds suggests it is trading at a 42% discount to its potential value.

Della Valle seems confident that after two years of flat growth, she can turn the group’s fortunes around in Germany, which will account for more than 30% of the group’s total sales after the recently agreed disposals in Italy and Spain. With an ageing population, the EU’s biggest nation hardly looks like a booming consumer market for data and internet usage. Vodafone however sees room to improve its operating performance in the country. And contrary to other European markets, Germany hasn’t been disrupted by new competitors eager to wage a price war, as Xavier Niel’s French startup Iliad did for example in Italy.

African subsidiary Vodacom’s revenue has meanwhile been growing a healthy 9%. Della Valle’s other growth hope lies in offering services such as information technology outsourcing or cybersecurity to corporate clients. That activity is seen expanding by 5% a year. The hope is to grow the segment from 30% to 50% of the group’s services revenue, in spite of the competition from industry incumbents who have been servicing corporates big and small for years. Based on today’s numbers, “mission accomplished” in that division would translate into over 7 billion euros of added sales, and a hypothetical 2 billion euros in extra EBITDA after leases based on the group’s current operating margin. That could add 10 billion euros in enterprise value, based on Vodafone’s 2025 multiple, helping to close the gap and offering comfort to investors such as Gulf technology company e&, which hiked its stake to about 15% since the Italian top executive took over.

Putting Vodafone back on the growth path will however take time. Della Valle’s shrinking job is mostly over. She has to switch to a sharper focus on improving operational performance, which may not yield immediate results, requiring investor patience. It took Della Valle just over a year to prune the decaying Vodafone tree. It will take longer before she can take pride in its fruits.

Updated 22:00 IST, May 2nd 2024