Published 14:41 IST, December 19th 2023

StanChart M&A theory will finally become reality

The London-listed lender has been the subject of M&A rumours for decades, with mooted suitors including Barclays, ANZ, and others.

- Republic Business

- 3 min read

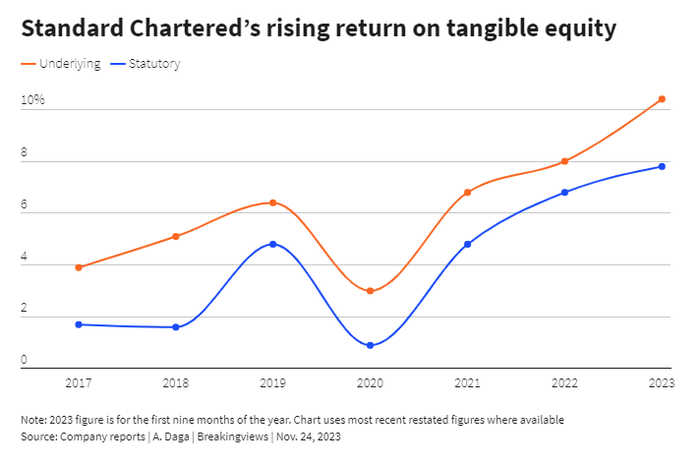

Through the winter. Things are finally going well for Bill Winters’ Standard Chartered. After a long period of anaemic performance, the Asia-focused lender generated a 10.4% underlying return on tangible equity in the first nine months of 2023, excluding a one-off impairment charge. But you wouldn’t know it from the share price. If that disconnect persists in 2024, long-running takeover theory may get real.

The London-listed lender has been the subject of M&A rumours for decades, with mooted suitors including Barclays, ANZ, and even the state-owned Chinese banking behemoths. First Abu Dhabi Bank (FAB) in early 2023 said it had studied a possible offer but was no longer doing so.

There are good reasons why a bid has never materialised. Start with StanChart’s global sprawl, which includes wholesale and retail-banking businesses and spans 50 countries in Asia, Africa, the Middle East and elsewhere. Very few possible acquirers would have an interest in bulking up in all those markets at the same time. The vast global footprint also means there are dozens of regulators and governments who could potentially make a takeover tricky.

What’s changed, however, is that StanChart’s long-standing discount now jars with the performance that Winters is churning out. Throughout much of 2023, the bank’s share price bounced around between 0.5 times and 0.6 times analysts’ average forecast for its tangible book value in 12 months’ time, LSEG data show. Historically, a low multiple was justified by low returns. But if the London-headquartered lender’s recent performance is sustainable, there shouldn’t really be a discount to book value at all. The upshot is that StanChart now looks attractively cheap, rather than deservedly so.

That could tempt FAB to take another look in 2024. A takeover would fit nicely with Gulf states’ ever more expansive corporate ambitions. Trade corridors are growing between the Middle East and Asia. A combination of the United Arab Emirates’ biggest bank and StanChart could form the financial backbone of these flows. Offering to divest businesses could ease regulators’ fears. It also helps that the 18% of StanChart owned by Temasek for more than a decade looks increasingly like a non-core holding. In theory, a would-be acquirer could sew up roughly one-fifth of the shares in one go by getting the Singapore state investor to tender.

Any bidder would have to be confident that U.S. authorities would allow the enlarged entity to keep StanChart’s dollar-clearing licence, which would be a bigger gamble for FAB than for Western lenders. Still, the gap between the bank’s valuation and its recent performance makes for an alluring financial combination, and boosts the chance that someone will finally pounce.

Updated 14:41 IST, December 19th 2023