Published 22:16 IST, April 22nd 2024

Swedes’ gaming split is far from a next-level fix

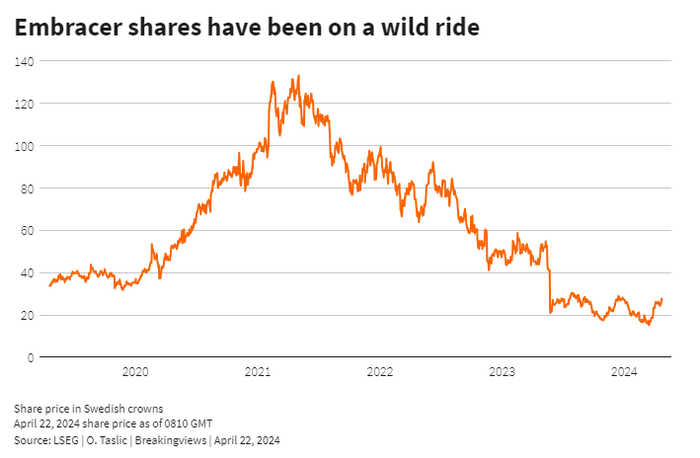

The company’s share price soared above 130 Swedish crowns in 2021 as it gobbled up competitors and Covid-19 lockdowns.

- Republic Business

- 3 min read

Coffee to go. Farväl, Embracer. The $3 billion Swedish video game company announced on Monday that it will split itself into three separately listed entities, with the remnant of the current group eventually changing its name. It’s a logical move for the exceptionally wide-ranging firm, which claims to have over 900 fully owned or controlled franchises. But it won’t necessarily create oodles of value for Embracer’s battered shareholders.

Embracer has had quite a ride. The company’s share price soared above 130 Swedish crowns in 2021 as it gobbled up competitors and Covid-19 lockdowns put rocket fuel under the video game industry. But the stock tumbled over 40% last year amid stuttering sales and the cancellation of a multibillion-dollar “development partnership”, prompting a radical restructuring and debt reduction programme.

The surgery announced on Monday takes that one step further: Asmodee, the board game giant behind “Catan” that Embracer acquired in 2022 for around $3 billion, will be a separately listed entity, alongside the peculiarly titled “Coffee Stain & Friends” – housing more mobile gaming and non-mainstream gaming assets – and “Middle-earth Enterprises & Friends”, a rump encompassing blockbuster console and PC games like those based on “Lord of the Rings” and “Tomb Raider”.

There’s a familiar corporate finance logic to the split. As CEO Lars Wingefors explained to analysts, investors will find it easier to choose between betting on steadier businesses such as Embracer’s board games, and swinging for the fences via the Middle-earth division. The latter’s blockbuster games cost much more to make but have a greater potential payoff, creating volatility that can act as a drag. Many of Embracer’s liabilities will now sit with the steadier Asmodee board games unit: a 900 million euro loan announced on Monday – and secured against Asmodee assets – will be used to help refinance the current group’s debt.

The optimists’ case would go like this. In 2023 Embracer’s mobile and niche gaming arm made $260 million of adjusted operating profit, while its Middle-earth business made $180 million. Putting both on a multiple of 12 – roughly what the sector trades at – and these two alone would be worth over $5 billion including debt. That’s more than Embracer’s $4.5 billion enterprise value as of December, and doesn’t even include the board games arm.

That vision is probably too cheery, though. Asmodee’s leverage will rise to 3.9 times adjusted EBITDA on a pro forma basis covering the 12 months to December 2023 – probably just about manageable, but riskier and thus meriting a discount. What’s more, volatile earnings in blockbuster gaming are currently offset by steadier business lines. This wouldn’t be the case if it was separately listed, which might also merit a discount.

Shareholders representing more than half of the capital and votes, including Saudi Arabia’s Savvy Games, have expressed approval for the breakup plans. Embracer shares also rose 10% in early trading on Monday. Yet to get a lot more enthusiastic – and in particular to get anywhere near Embracer’s previous $8 billion-plus valuation – Wingefors will need to do more than reshuffling the pack.

Updated 22:16 IST, April 22nd 2024