Published 14:55 IST, March 28th 2024

Tata’s forced IPO will only bring problems

Tata Sons, overseen by Chair Emeritus Ratan Tata houses the group's stakes in around 14 listed companies.

- Republic Business

- 3 min read

Charity begins at home. One of India's biggest family businesses is in an pickle. Tata Group, the sprawling cars-to-tech conglomerate, is hurtling towards a forced listing of its holding company that would lump it with a yawning market discount. And if that wasn't bad enough, scrutiny that comes with an initial public offering could create other problems too.

Tata Sons, overseen by Chair Emeritus Ratan Tata, is vast. It houses the group's stakes in around 14 listed companies, including Tata Consultancy Services, Jaguar Land Rover-owner Tata Motors and Tata Steel. It also owns unlisted businesses such as Air India and others that tap into India's high-tech manufacturing ambitions; privately-held Tata Electronics, for example, assembles iPhones for Apple and is building a big semiconductor fabrication facility in Dholera, Gujarat.

All of that may soon be shoved into the public eye. Around 18 months ago the central bank categorised Tata Sons as an "upper layer" non-bank financial company. That effectively required it to list within three years. So its deadline for a debut, September 2025, is approaching. Speculation is starting to pick up about how much the company might be worth.

The Reserve Bank of India's intentions are good. It is eager to avoid a repeat of the failure of Infrastructure Leasing & Financial Services. The default in 2018 of that shadow bank with debt of over $12 billion sent markets into a panic and triggered a liquidity crisis that caused prominent businesses to collapse.

Tata Sons appears to be preparing for action. It raised $1 billion last week by selling some of its 72% stake in Tata Consultancy. It could use those proceeds to trim debt to clean up the holding company ahead of floating it. It's unlikely that tidying up the balance sheet would be enough to avoid a listing altogether, however.

In total, Tata Sons’ holdings might be worth $194 billion. Its listed stakes alone amount to $187 billion per Breakingviews calculations, and analysts at Jefferies estimate a book value of almost $7 billion for the rest. If fully valued by the markets, and not factoring in any debt, Tata Sons would rank as India's second largest listed company after Mukesh Ambani's $244 billion Reliance Industries.

Yet a full valuation is unrealistic. Indian entities suffer from high holding company discounts. The figure averages 67% across major sectors, according to research firm Incwert. The discount would be hard to swallow for a group like Tata that has painstakingly listed its individual companies to avoid such value gaps and kept other businesses private so that it can incubate them. By contrast, Ambani houses his oil-to-retail empire under one listed entity.

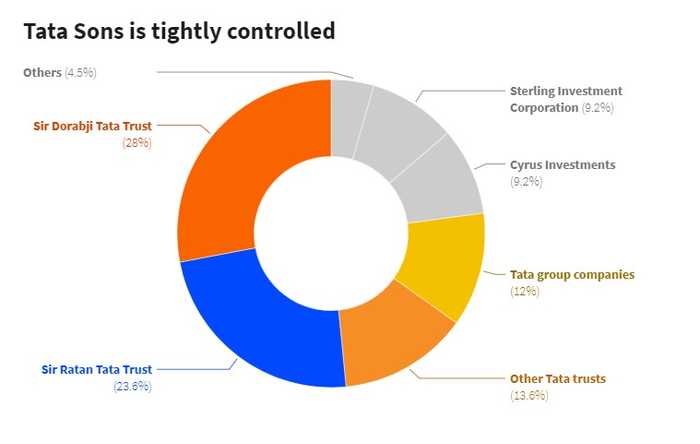

The final wrinkle is possibly the most complicated. A listing of Tata Sons could impact the entity's ultimate owners. Two-thirds of the holding company is owned by a network of charitable trusts that run cancer hospitals and give out education scholarships among other things. Some of them are more than a century old and, for that reason, have exemptions that allow them to own shares in companies without tax implications.

Those exemptions have been challenged in the past, however. Tata has twice beaten India's tax administrators in court. Globally, Rolex, Ikea and Carlsberg are owned or controlled by charities. But such structures aren’t common in India.

One potential worry is that Tata Sons' listing will highlight the special treatment its owners receive, and whether that is still deserved. Any fresh challenge on that front could force another restructuring even higher up.

Updated 14:55 IST, March 28th 2024