Published 19:11 IST, April 28th 2024

Thoma Bravo UK cyber deal looks a little too good

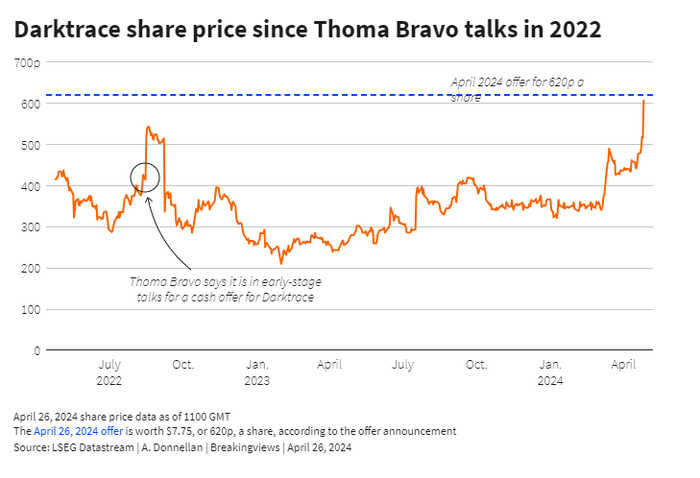

Thoma Bravo was keen on scooping up Darktrace as far back as 2022, but the approach fell apart after an unhelpful leak.

- Republic Business

- 2 min read

Shot in the dark. U.S. private equity group Thoma Bravo seems to have cracked the buyout code with its $5.3 billion acquisition of Darktrace. On Friday, the two sides announced that they had agreed a deal, after previous talks collapsed. The only wrinkle is that the returns on offer for Thoma Bravo look good – perhaps uncomfortably so for shareholders in the UK cybersecurity outfit.

Thoma Bravo was keen on scooping up Darktrace as far back as 2022, but the approach fell apart after an unhelpful leak. Fast forward to 2024, and Darktrace’s shares are on the up, thanks to CEO Poppy Gustafsson’s nascent push into the giant U.S. market. They were bouncing around between 3 pounds and 4 pounds per share in the summer of 2022, around the time of the last talks, but have recently been closer to 5 pounds. Thoma Bravo’s dollar-denominated offer slaps another roughly 40% on top of that, valuing Darktrace at 6.19 pounds per share, using Friday’s exchange rate. The company has also successfully distanced itself from co-founder Mike Lynch, who is on trial in the U.S. for fraud, which he denies.

Chunky premium notwithstanding, Thoma is looking at a juicy return. Strip out net cash, and the offer gives Darktrace an enterprise value of just under $5 billion, or 34 times 2023 EBITDA. Assume that the new software-specialist owner manages to boost sales by 20% a year for five years, roughly in line with analysts’ current forecasts, and keeps the EBITDA margin steady at 24%. By 2028, EBITDA would be $363 million. Apply the same valuation multiple, and the enterprise would be worth $12.4 billion. In other words, Thoma can more than double its money just by doing what analysts think the business will do anyway in the coming years. That’s based on Breakingviews calculations which conservatively assume no debt financing.

Any success in the U.S. market could deliver an even greater return. Darktrace’s $72 billion rival CrowdStrike will grow at roughly 30% in the coming years, analysts reckon. Assume the same for Darktrace, and Thoma could quadruple its equity cheque by 2028.

So far, 14% of Darktrace’s shareholders, including former owner KKR, have given their backing to the deal. Given Thoma’s scope for success, other shareholders have a reason to ask for more.

Updated 19:11 IST, April 28th 2024