Published 20:52 IST, March 19th 2024

Unilever’s sweet exit comes with sour aftertaste

Unilever has a stranded assets problem but ice cream brands like Twister and Feasts look vulnerable to sugar taxes.

- Republic Business

- 3 min read

Tooth ache. “I scream, you scream, we all scream for ice cream”. Not at Unilever headquarters though, where the days of this particular earworm are numbered. On Tuesday, the 99 billion pound ($126 billion) consumer goods company announced a plan to spin off the division that makes Ben & Jerry’s, Cornetto and Magnum sweet treats. CEO Hein Schumacher is doing the right thing, but it leaves his investors with an unfortunate aftertaste.

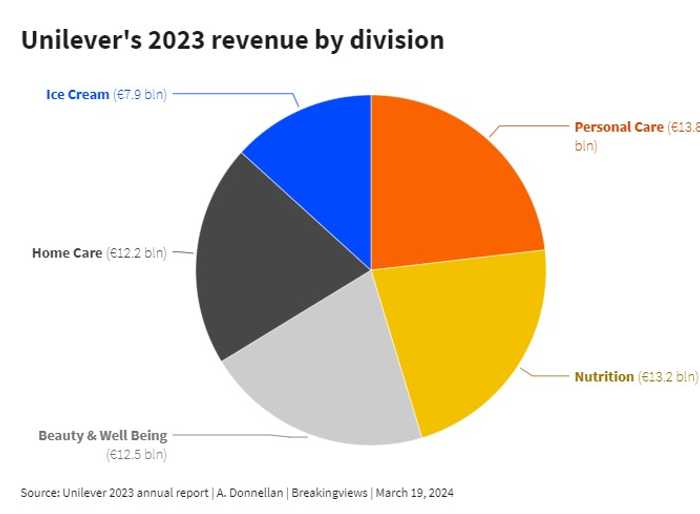

Right now, Unilever has a stranded assets problem. Ice cream brands like Twister and Feasts look vulnerable to sugar taxes and other regulations from governments keen on improving the overall health of their populations. Offloading a division that delivered sales nearing 8 billion euros in 2023, 13% of the group’s overall level, makes a handy dent in said problem. Based on 2023 annual results, edible items will soon only constitute 25% of revenues and the group will be more focused on beauty, personal care and hygiene products like Dove soap, Persil washing powder and Comfort fabric softener.

The good news can be quantified, too. Before Tuesday Unilever’s assumed 3% to 5% growth in sales in the coming years. As a result of hiving off ice cream, Schumacher now envisages “mid-single digit growth”, and reckons the plan will “support margin improvement over time”. He also won’t have to deal with sticky governance situations like those created by Ben & Jerry’s independent board.

His shareholders may still feel queasy, though. Disentangling the ice cream arm from Unilever’s sales and marketing operations in 57 geographies creates duplicated human resource and legal costs. The group is planning 800 million euros of cost savings mainly from cutting 7,500 head office roles globally, but it’s a reminder that breakups cost money. That would be fine if Schumacher was selling the business to a new owner who was advancing a premium for the privilege. But a spinoff just means handing each investor a new share, meaning they’re shouldering the expense themselves.

Admittedly, Unilever shareholders may not find simultaneously owning a massive ice cream group too much of a downer. With 800 million euros of operating profit last year, the group would be worth 10 billion euros if it traded on the same 2023 multiple as Unilever itself, and still be a chunky player even at a discount. With most of its sales in the United States, a New York listing could fetch a higher valuation than a London one given U.S. investors are less fixated with environmental, social and governance preoccupations.

All that said, even after its split Unilever will remain a major food player. Rivals like $379 billion Pampers diaper maker Procter & Gamble and beauty giant L’Oréal aren’t. That may be one reason why P&G is valued at nearly 24 times its 2024 earnings and L’Oréal trades at 34 times, while Unilever languishes on 16 times. To narrow the gap, Schumacher may have to split out more edible stranded assets.

Updated 20:52 IST, March 19th 2024