Published 18:29 IST, April 20th 2024

Winner’s curse unfairly haunts $7 bln paper deal

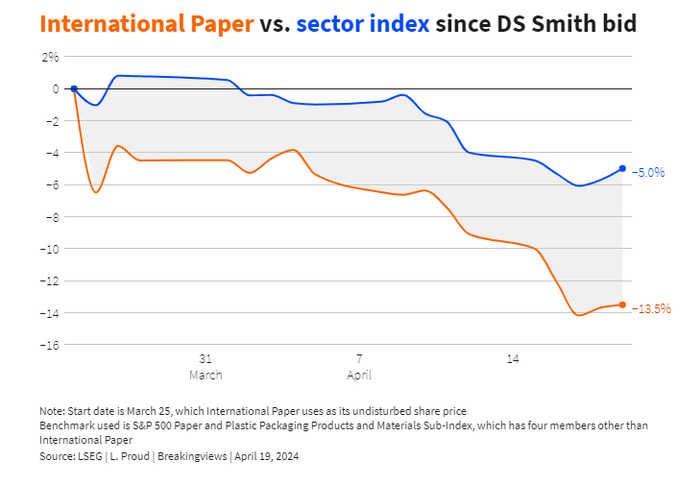

The worry for International Paper chair and outgoing CEO Mark Sutton is that investors seem wary.

- Republic Business

- 2 min read

Through the mill. Chunky acquisitions tend to destroy shareholder value, numerous studies have found. It’s therefore understandable that investors often take fright when a company they own launches a takeover bid. Sometimes that scepticism obscures a good thing, however – as International Paper’s purchase of UK-listed packaging peer DS Smith might show.

The transatlantic pairing, agreed on Tuesday, was sealed on Friday when rival bidder Mondi dropped out of the race. The Memphis, Tennessee-based victor is handing DS Smith investors 0.1285 of its own shares in return for each one they hold of the target’s, implying an equity offer of almost $7.4 billion based on undisturbed share prices.

The worry for International Paper chair and outgoing CEO Mark Sutton is that investors seem wary. His share price is down by more than a tenth since March 25, the last trading day before the public approach. That’s reduced the real premium on offer for DS Smith to 30%, rather than the original 48%. The rest of the paper and packaging sector has dropped, but not by as much as the acquiror.

The slide is arguably surprising since the combination will create annual cost savings of around $500 million, according to International Paper. Those synergies have a net present value of $3.4 billion, based on Breakingviews calculations using a 25% tax rate, 10% discount rate and the buyer’s estimated integration costs of $370 million.

True, Sutton is effectively paying away two-thirds of that value to DS Smith since the undisturbed bid premium over the target’s share price was equivalent to about $2.4 billion. But there should still be about $1 billion worth of goodies left for International Paper itself. Sutton’s shareholders seem not to believe it.

Investors may see the cost-cut estimate as overcooked, or they may mistrust cross-continental empire building. Even if only two-thirds of the synergies came through, however, International Paper’s return on the investment would be about $950 million in four years’ time, using Visible Alpha consensus operating profit estimates for DS Smith of $935 million and a 25% tax rate. That’s a near-10% return on investment. Assume all the synergies materialise, and the return is a handy 11%.

It’s worth considering the alternative. Peers like Smurfit Kappa and WestRock are pairing up, in a sector that generally rewards scale. Forgoing a deal, for International Paper, would come with risks of its own. At least Sutton hasn’t left himself strategically boxed in.

Updated 18:29 IST, April 20th 2024