Published 18:27 IST, November 2nd 2023

Larry Fink’s next M&A may go in surprise direction

Larry Fink, BlackRock's CEO, aims to make a transformational deal before retiring at 71.

- Opinion

- 6 min read

Finicky. BlackRock may be the world’s largest asset manager, but founder Larry Fink still feels he has something to prove. The $89 billion company’s chairman and CEO, who turns 71 on Thursday, is eyeing retirement and grooming potential successors. But he also wants to do a transformational deal before vacating the corner office. While the possibilities are many, options with real traction are few. One in particular would take Fink in a surprising new direction.

Larry’s tradition

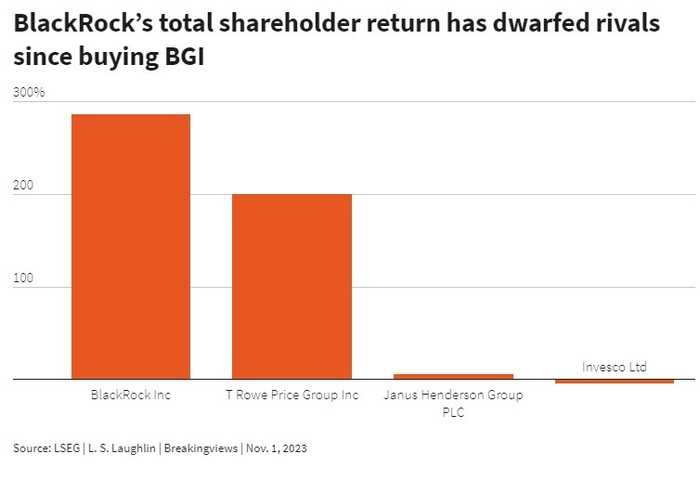

The former First Boston banker founded BlackRock in 1988 with help from private equity firm Blackstone, which took a 50% stake. Its subsequent growth into a global behemoth owes much to Fink’s audacious acquisitions. He absorbed Merrill Lynch’s asset management arm in 2006. Three years later, after the global financial crisis, he bought Barclays Global Investors from the British bank for $13.5 billion.

That transaction was the cornerstone of BlackRock’s exchange-traded funds business which fueled the firm’s growth as investors shifted to investment products with lower fees. Over the next decade, BlackRock outperformed rivals like T. Rowe Price, Invesco and Janus Henderson. On the firm’s most recent earnings call, Fink noted that mergers, including BGI specifically, were the “foundation of the firm”. He shows no sign of losing his taste for a deal: BlackRock executives considered participating in a rescue of Credit Suisse earlier this year shortly before the Swiss bank’s sale to rival UBS.

Tipping the scales

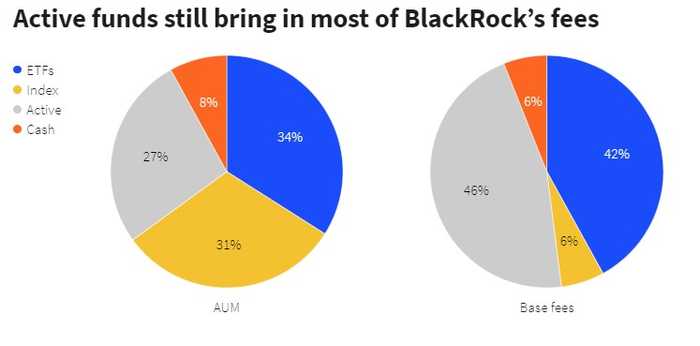

The shift to low-fee products helped BlackRock’s assets under management swell to more than $9 trillion at the end of September. However, it is not immune to the pressures facing the broader fund management industry. Actively managed funds accounted for 27% of its assets in the third quarter but brought in 46% of its fee income. Though the firm’s size offers enormous economies of scale, it faces relentless pressure to keep lowering costs.

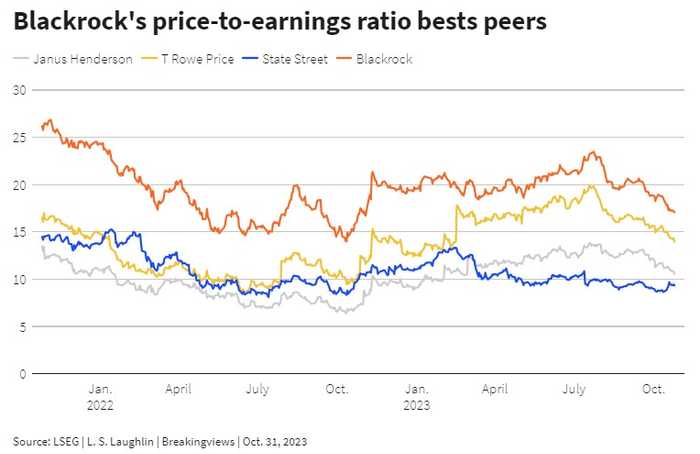

BlackRock’s adjusted operating margins of 42% in the last quarter may be the envy of many rivals, but they are 5 percentage points lower than in the same period two years earlier. Investors are moving assets out of equities and into fixed income to take advantage of higher interest rates, and debt funds tend to charge slimmer fees. In other words, BlackRock could use a new growth engine.

One option is for Fink is to get even bigger in asset management. In theory, BlackRock could absorb a traditional firm like, say, $20 billion T. Rowe Price or $6 billion Invesco, cut costs and create value through improved efficiency. BlackRock’s higher valuation gives it an acquisition currency.

The problem is that Fink can continue to nab assets organically without the risks associated with a deal. Accumulating more fund management assets will also draw greater attention to BlackRock, which already holds a sizeable chunk of most listed companies on behalf of its clients.

Angling for an alternative

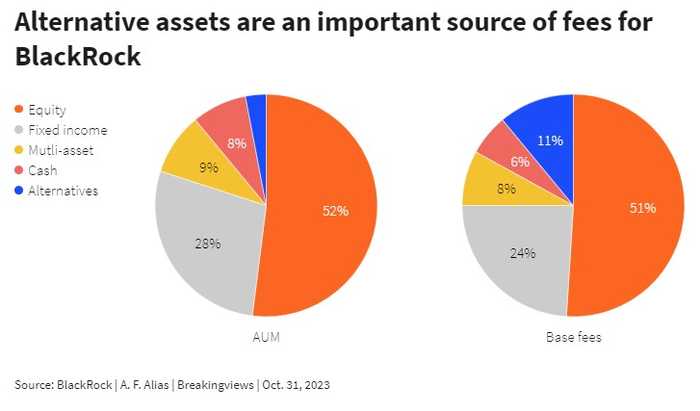

Another option is for BlackRock to bulk up in the fast-expanding market for private assets such as leveraged buyouts. The firm has benefited from growing demand for unlisted investments, where fees are juicer: BlackRock’s alternatives group last quarter brought in 11% of its parent’s total asset management revenue despite overseeing just 3% of funds. BlackRock’s history with Blackstone means a reunion with Stephen Schwarzman’s $110 billion firm is a persistent Wall Street rumor.

There’s room for BlackRock to improve in this business which one analyst describes as “subscale”. But any deal would also come with hefty baggage. Buyout professionals tend to be highly paid rainmakers. Tacking that culture onto BlackRock’s efficient machine could create a clash.

BlackRock’s funds operate under a single name, so uniting with Carlyle or Apollo Global Management would pose a branding challenge. BlackRock’s asset-light balance sheet would also appear to rule out a deal with the likes of the $46 billion Apollo, which has its own insurance unit.

Plumbing the index

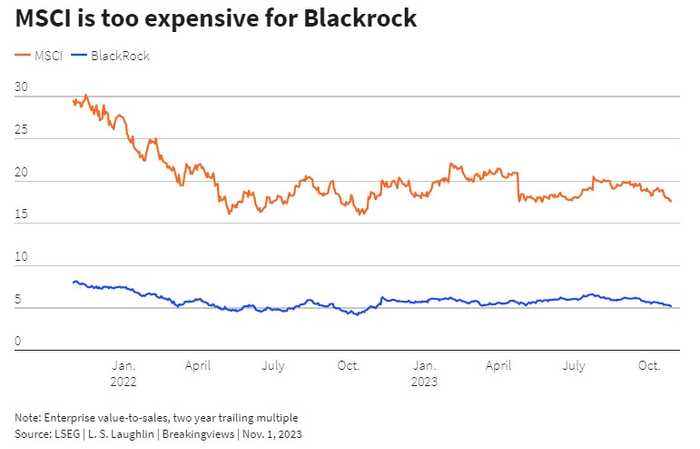

Another option is to expand into an ancillary business. As a leading purveyor of index funds, there’s some logic for BlackRock branching out into the business of compiling stock indices. Fink might covet MSCI, the $38 billion firm which aggregates many of the benchmarks tracked by BlackRock’s ETFs. A deal would yield immediate efficiencies: in 2022, BlackRock paid MSCI more than $200 million, accounting for more than 10% of the company’s revenue. The problem is price. Including debt, MSCI is valued at around 18 times last year’s revenue, three times BlackRock’s multiple.

On the recent earnings call, Fink noted that he was challenging his team to think more broadly about technology M&A. The company’s revenue from technology services in 2022 was $1.4 billion, about double what it was in 2018. The unit includes BlackRock’s Aladdin platform, an interface that offers large institutional clients a breakdown of the risk in their portfolios, including private markets.

There are only so many companies that would offer BlackRock a sizeable transaction. One is the London Stock Exchange Group, which has transformed itself into a data provider after acquiring Refinitiv, a former unit of Thomson Reuters, owner of Breakingviews.

Take that thinking a half step further and it brings Fink closer to another soon-to-be-retired New York entrepreneur: Michael Bloomberg, owner of the eponymous financial news and data provider. Its terminals pump out stock prices for risk analysis, plus Bloomberg has an index platform. It has a technology base, and, in the United States, a near-monopoly on trading floors. While it’s hard to find a Wall Street executive who doesn’t bellyache about the price of a Bloomberg terminal, it’s even harder to find one who won’t pay for it. That’s the sort of pricing power Fink may covet.

Bloomberg, who has always resisted selling, may have a hard time giving it up to Fink. Even if the former New York mayor agreed to part with his business, a deal would come at a steep price. The company generated more than $12 billion in revenue in 2022, according to the New York Times. At a multiple of eight times that figure – a modest premium to rival LSEG – Bloomberg would be worth more than BlackRock.

Yet even if the idea sounds loony, it’s one that is doing the rounds behind closed doors. Given Fink’s long record of pulling off opportunistic and transformational deals, it would be foolish to bet against him springing one last surprise.

(Source: Reuters Breakingviews)

Updated 18:27 IST, November 2nd 2023