Published 20:53 IST, April 16th 2024

Microsoft-backed IPO breaks rule of 40 at bad time

Founded in 2013, Rubrik is in the business of protecting data, analyzing threats.

- Opinion

- 3 min read

Rebel. Rubrik is attempting to rewrite the rules of success. The Microsoft-backed cybersecurity firm filed to go public in early April flaunting a useful metric used to determine the success of faster-growing technology firms. The window for initial public offerings is tentatively cracked open, but investors are more discerning. It’s a tough time to buck the norm.

Founded in 2013, Rubrik is in the business of protecting data, analyzing threats, and helping organizations recover from cyberattacks. It counts over 6,100 enterprise customers including Home Depot , Pepsi and Goldman Sachs. And its relationship with Microsoft has been helpful. “Ruby” – its artificial intelligence unit – enlists the $3 trillion tech giant’s help with software.

Much like Microsoft’s model, the company led by Bipul Sinha recently pivoted away from licensing agreements and toward a subscription-based cloud computing business. The change is reflected partly in its top line: Revenue tied to licenses more than halved in the fiscal year ending January 2024, but subscription revenue increased 40% during the same period.

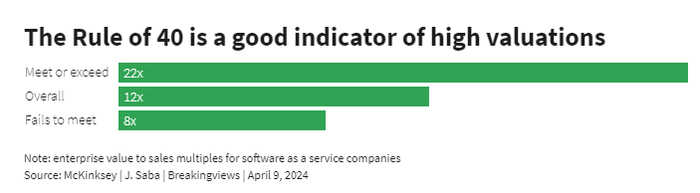

Nonetheless, Rubrik is part of the software as a services (SaaS) club, a group that largely adheres to the Rule of 40. The metric combines a company’s revenue growth rate plus its free cash flow as a percentage of sales. If the two add up to more than 40, it’s a good indicator that a high valuation is warranted. In a study by McKinsey that analyzed SaaS companies, those that matched or exceeded the rule had enterprises that were worth 22 times sales, or roughly three times the multiple of those companies that didn’t. If Rubrick justified the higher valuation, it would be worth $14 billion, more than triple what it was valued at when Microsoft paid for a stake in 2021, according to Bloomberg.

Yet it is nowhere near the Rule of 40. Overall revenue increased just 5% for the year ending January 2024. Rubrik’s cash burn has increased, from negative $15 million in fiscal 2023 to negative $24 million for the most recent year. Losses are widening.

Meanwhile, investors are tightening their standards. In 2021, the median SaaS company that went public fell short of the Rule of 40 with a score of 36, according to data from investment firm Iconiq. Almost 80% of those companies are now trading below their IPO price. On McKinsey’s average multiple of 8 times sales for those companies whose growth and free cash flow fall short, Rubrik’s enterprise value based on last year’s revenue would be $5 billion. That is approximately the valuation the Palo Alto, California-based company is aiming for, according to an updated U.S. regulatory filing on Tuesday. With shareholders more focused on the earnings it lacks, Rubrik is right to lower its value expectations.

Updated 20:53 IST, April 16th 2024