Published 16:37 IST, December 20th 2023

BP and Equinor will find common ground

A tie-up of BP and Equinor could generate synergies worth $4.8 billion a year on combined 2024 revenue of $317 billion, per LSEG forecasts.

- Republic Business

- 4 min read

Better together. Mega-mergers have strengthened U.S. oil majors Exxon Mobil and Chevron and revived talks of more cross-border M&A. One player looks potentially vulnerable: Britain’s BP, worth around $100 billion at the end of November. Its valuation is depressed and the abrupt departure of former CEO Bernard Looney has created a leadership void. Daring to merge with similarly sized Norwegian ally Equinor may allow BP’s next boss to both protect and strengthen the UK group.

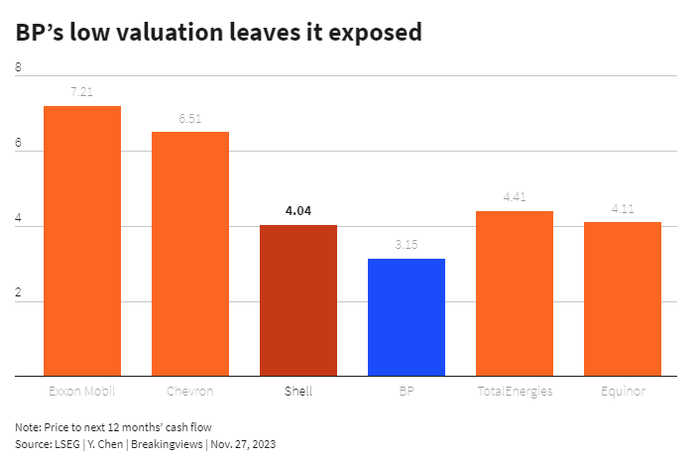

European energy companies were trading at a nearly 50% discount to U.S. rivals on a price to cash flow basis in November. But BP’s particularly cheap valuation and fragmented ownership could turn it into a hostile takeover target. Its market valuation slipped to just 3 times its cash flow for the next 12 months, well below the 4 times fetched by Equinor, larger British rival Shell and French competitor TotalEnergies, LSEG data show. Also, Equinor had over $10 billion in net cash at the end of September, while these two rivals held more debt than cash.

Working on a defence strategy by capitalising on existing business ties would make sense. In 2020 BP became a green partner to Equinor through the $1.1 billion acquisition of a 50% stake in its U.S. offshore wind projects. The duo has also stood out as planning to spend more than rivals on low-carbon assets: BP has pledged to invest between $7 billion and $9 billion a year by 2030 in businesses including electric-vehicle charging, biofuels and hydrogen. That would be equivalent to half of its projected annual capital expenditure, up from 30% in 2022. At over 50%, Equinor’s non-oil spending target is similar. TotalEnergies, in comparison, expects to devote only about a third of its capital to low-carbon ventures. Finally, BP Chairman Helge Lund, who led Statoil – before it was renamed Equinor – for a decade until 2014, provides the UK group with a strong Norwegian connection.

A merger would bring financial benefits. Shell’s purchase of BG Group led to annual pre-tax savings of $4.5 billion, or 1.5% of their 2015 revenue. On that basis, a tie-up of BP and Equinor could generate synergies worth $4.8 billion a year on combined 2024 revenue of $317 billion, per LSEG forecasts. Through BP, Equinor would gain a bigger international footprint and greater exposure to the lucrative liquefied natural gas segment and green industries in the U.S. and Asia. This would help the Norwegian major to diversify away from gas pipeline exports to Europe, which are set to shrink. Equinor would also take on BP’s much larger oil trading arm.

BP, meanwhile, would be in a stronger position to keep investors happy. The UK company has pledged to return 60% of its surplus cash flow to shareholders. Equinor’s high-margin Norwegian oil and gas operations could boost payouts and provide capital for green investments.

There’s one major hurdle. The Norwegian state, which owns 70% of Equinor, may be reluctant to lose majority control. Yet a transaction in which the Scandinavian group offered a 30% premium through shares and some $10 billion in cash would see Oslo remain the top shareholder with around a third of the enlarged company, Breakingviews calculates. That would give Norway enough heft to control the board and block unwanted strategic moves. Elsewhere in Europe, the Italian and Finnish states hold 32% and 36% respectively in national champions Eni and Neste. Paris cut its stake in TotalEnergies to less than 1% in the 1990s.

If Lund can make a strong case at home, a $200 billion-plus European energy major with a shared climate vision could become a reality.

(This is a Breakingviews prediction for 2024. To see more of our predictions, here.)

Context News

BP announced on Sept. 12 that CEO Bernard Looney had resigned with immediate effect after admitting he hadn’t been “fully transparent” about past relationships with employees. Murray Auchincloss, the company’s CFO, has been since acting as interim CEO while the company seeks a permanent solution. Chairman Helge Lund, who ran Statoil – before it was renamed Equinor – for 10 years until 2014, favoured an internal hire in the aftermath of Looney’s departure, but no preferred candidate has emerged 10 weeks later, according to people with knowledge of the process, the Financial Times reported on Nov. 24. BP said both internal and external candidates were being considered in the search for a permanent replacement.

Updated 16:37 IST, December 20th 2023