Published 20:58 IST, January 4th 2024

Red Sea windfall will only delay shippers’ pain

Shipping groups are re-routing major trade lanes around Africa’s Cape of Good Hope.

- Republic Business

- 3 min read

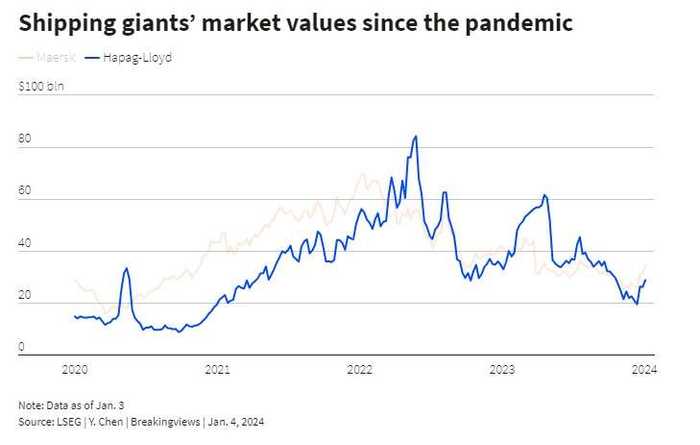

Pain killer. Yemen’s Houthis are stirring up the Red Sea and shipping company investors. Denmark’s Maersk and Germany’s Hapag-Lloyd, for example, have gained some $18 billion in market value since mid-December, as militant attacks shut the Suez Canal, causing freight rates to double. Yet hopes for a lasting boost may be disappointed.

Maersk this week decided to shun the Suez Canal indefinitely, where 12% of global trade passes through. That’s after one of the $35 billion group’s vessels narrowly escaped a hijacking thanks to U.S. helicopters, in turn prompting Iran, which backs the Houthi rebels, to send in a warship. As a result, shipping groups are now re-routing major trade lanes including the Asia to Europe traffic around Africa’s Cape of Good Hope, which adds at least 10 days of travel time.

The extra time and riskiness of the journey has caused freight rates to soar. Asia to Europe prices, for example, have nearly doubled since mid-December to more than $4,000 per forty-foot equivalent unit (FEU), Freightos data showed as of Jan. 3. While that’s still a far cry from the more than 10-fold increase during the pandemic, the result should be a windfall for shipping groups.

Take Maersk. If current freight prices are sustained throughout the year, the Danish group’s 2024 operating profit could rise by $12 billion, according to Breakingviews calculations which assume that each $200 increase in FEU costs brings in $1.2 billion of extra EBIT. To justify the $8 billion jump in market capitalisation, and an equivalent rise in 2024 net income, prices would need to stay at current levels for over nine months, assuming a tax rate of 22%.

There are reasons to think they may peak sooner. Chinese factories are working around the clock before the week-long Lunar New Year holiday in February, keeping ships busier than usual. Global demand is also weakening.

And, unless the conflict in Gaza escalates across the region, there is likely to be a concerted international effort to reopen the canal. Annual freight contracts are cheaper than the spot market, according to one market participant, implying that prices are expected to fall.

When the boon fades, companies like Maersk and Hapag-Lloyd will still have to grapple with the legacy from the pandemic. Port congestions and quarantine requirements pushed up freight prices, taking Maersk’s operating margin to 40% in 2022. But it also led to higher costs and over-investment in ships, which ultimately hurts prices. The percentage of idle fleets averaged around 4% last year, according to Alphaliner data. And a record number of vessels coming online in 2024 could add some 12% to total shipping capacity, Barclays analysts reckon. Maersk and Hapag-Lloyd shares have fallen by half and two-thirds since the peak in 2022. The Red Sea crisis may provide only a temporary relief.

Updated 20:58 IST, January 4th 2024